Beyond Growth: What Matters for Value Creation in AI

Lessons from Cursor's $60B acquisition

Cursor has had one of the most dramatic public consensus arcs in AI. Just 1.5 years ago, it was celebrated as the first breakout AI application company. Then Anthropic launched Claude Code, quickly gaining momentum, and later OpenAI launched Codex.

Suddenly, the market narrative became: “Cursor is dead.” The argument was simple: how can an AI application startup survive when the two frontier labs — valued at ~$2Tn combined — decide to compete directly, head to head?

Then SpaceX announced it would acquire Cursor for $60B — the largest venture-backed startup acquisition ever.

I’m not a developer, so I don’t personally feel the magic of AI coding products. But as an investor who’s invested across all stages from pre-seed to public-market stocks, what I found most fascinating is what we can learn about value creation in AI — using Cursor as a case study.

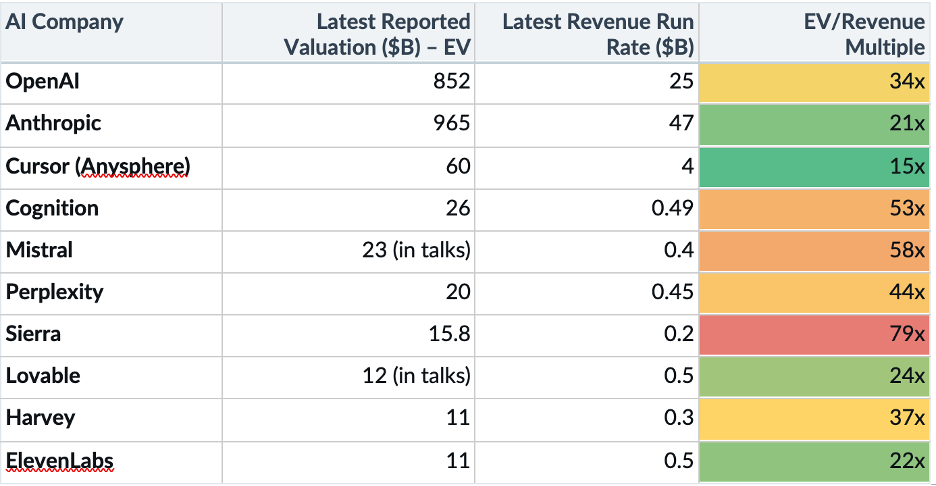

How are leading AI companies being valued today?

At the highest level, valuation (EV) of any company is driven by two things:

Growth (and the long-term durability of growth)

Margin

Cursor’s $60B price tag sounds almost crazy at first glance.

But if you look at its latest reported ARR of $4B, the acquisition values Cursor at about 15x ARR. Suddenly, the number looks much less crazy.

Note this is not meant to be a perfect comp table, as reported valuations and revenue run-rates are approximate and change quickly. The goal is to provide a ballpark picture of how the market values today’s leading AI companies.

Even at first glance, Cursor’s 15x EV/Revenue multiple looks shockingly low — far lower than the other AI application companies on this list.

Typically, a lower multiple is explained by slower growth — but that was not the case for Cursor. In fact, Cursor has one of the fastest growth rates among AI application companies, going from $100M to $4B (so 40x!) in only 1.5 years.

So the question becomes: why?

Because even though Cursor has very impressive growth, the market is discounting two things: durability and margin.

1. Growth: the opportunity is enormous but durability is uncertain

The first lesson from Cursor is that AI applications can create revenue at a speed we have rarely seen in technology before.

This is what makes the application layer so exciting. When the product works, not only can adoption be incredibly fast, but real revenue growth — both B2C and B2B — can be through the roof.

What about competition?

Cursor’s share of AI coding tool spend reportedly fell from 41% in June 2025 to 26% in May 2026, according to Ramp data.

Yes, this is bad news for Cursor, and hence the doubt about long-term durability.

But losing share while maintaining insane revenue growth is only possible in one kind of market: an exploding one.

A big part of that is the sheer size of the market. If we size Cursor’s TAM as the software engineering labor pool itself, that is a $2–3 trillion market.

There are ~20–30 million professional developers worldwide. In the U.S., the median annual wage for software developers is ~$133K.

Using this TAM for AI coding tools, Cursor’s $4B revenue run rate today shockingly still represents less than 1% of the market.

And this explains why all three players — Cursor, Claude Code, and Codex — can grow rapidly all at the same time. The market is simply too large and too early.

This reminds me of Stripe.

Today, Stripe is valued at over $150B and processed $1.9Tn payment volume in 2025 — yet it still captures only 5% of the global digital payment volume market.

That is what large markets do. They allow multiple excellent companies to grow for a long time, even when the competition is intense.

But growth is only the first part of value creation.

2. Margins: the economics are still unproven

While most people have focused their attention on competition, another red flag for Cursor — one that is much less reported — is gross margin, the basic economics of the business.

In the previous Internet and SaaS era, we were used to companies losing money.

When I was at Fidelity meeting companies on their IPO roadshows, I remember seeing many red numbers in operating losses.

But the biggest difference is that SaaS companies have high gross margins (~80–90%), and then they spend aggressively on sales, marketing, product, and engineering to continue their fast growth, before choosing to slow down internal investments and become profitable.

AI applications are different.

Cursor had negative gross margin up until Jan 2026, and only recently turned gross-margin positive.

For many AI application companies, the cost of serving each user can be very high because compute and inference costs sit directly inside cost of goods sold. Cursor relied heavily on third-party frontier models — reportedly paying Anthropic more than its own revenue at one point, a big contributor to those negative margins.

For Cursor to build a sustainable long-term business, it has to reduce its cost of goods sold and drive up gross margins.

That means relying less on expensive frontier models, building or fine-tuning its own models, leveraging open-source models where possible, and routing tasks intelligently across models with different cost and performance profiles.

Cursor clearly has realized this, and this explains its launch of Composer as its own coding model. If Cursor can use open-source foundations, reinforcement learning, domain-specific training, and product-specific context to deliver a great coding experience at much lower cost, then it has a path to better gross margins.

But this is a difficult balance: you cannot cut costs if it makes the product worse, because the magic of these products is the user experience — often tied to model capabilities. This applies to Cursor and every other AI application company.

Even OpenAI and Anthropic are intensely focused on improving compute efficiency and inference economics. For AI application companies, the pressure is even higher because they are paying frontier labs for intelligence, in addition to all the other costs.

As such, gross margin remains one of the biggest open questions (and challenges) for AI companies.

What are the lessons for AI value creation?

Cursor shows both the promise and the tension of the AI application layer.

The promise: AI applications can go from zero to billions of dollars of ARR faster than almost anything we have seen in technology history.

The tension: revenue growth is not enough. To build a long-term sustainable business (creating long-term enterprise value), Cursor needs to answer more questions around margins and long-term durability.

Growth gets you into the game. Margins determine whether the business model works. Durability determines whether the company has the right to win long-term, and this is the foundation of value creation.

The next generation of iconic AI application companies will not just be the ones that grow the fastest at the moment.

They will be the ones that prove the durability of their growth, bend their cost curves down, and win either on ROI (better cost and speed) or on depth (deep embedding into customer workflows) — enough that neither the frontier labs nor other application startups can easily displace them.

That is where the next generation of AI enterprise value will be created.